Small businesses, SMEs and mid-sized companies are increasingly faced with a proliferation of ESG questionnaires: tender processes, credit applications, supplier assessments, and more. Each stakeholder requests its own set of information, creating a significant administrative burden for organisations that often lack dedicated teams or appropriate reporting tools.

Yet, this information is essential. It enables organisations to assess their contribution to sustainability challenges, strengthen transparency, and foster stronger relationships with financial partners.

What if the solution lay in the voluntary adoption of a simple, recognised and structuring framework: the VSME standards (Voluntary Standard for non‑listed micro‑, small‑ and medium‑sized undertakings)? Could they become the future reference framework for lenders, contracting authorities and investors, while also delivering tangible benefits for the ecological transition?

Willing analyses the foundations, challenges and opportunities associated with these new reporting standards.

The origins of VSME: a pragmatic response to the CSRD

The European Union introduced the Corporate Sustainability Reporting Directive (CSRD) to regulate non‑financial reporting across environmental, social and governance (ESG) matters.

However, the CSRD was widely viewed as overly complex for SMEs and mid-sized companies. As a result, an Omnibus Directive was adopted in 2025, narrowing the scope of the CSRD and exempting a large proportion of companies. The revised thresholds limit mandatory application to organisations with more than 1,000 employees and €450 million in turnover.

While a large majority of French companies now fall outside the scope of the CSRD, they must nevertheless continue to respond to the ESG questionnaires of their partners. The challenge, therefore, is to strike the right balance between reliable, decision‑useful reporting and operational pragmatism.

Following this decision, EFRAG (European Financial Reporting Advisory Group) developed the VSME standards, specifically designed for mid‑sized companies, SMEs and very small enterprises. These standards form an integral part of the CSRD framework but, unlike the Directive itself, they are voluntary rather than mandatory.

The VSME standards pursue three clear objectives:

- To inform stakeholders, enabling them to make well‑founded decisions on companies’ sustainability profiles;

- To improve the company’s sustainable performance;

- To contribute to a more sustainable and inclusive economy.

VSME: a simple, progressive framework tailored to small and medium‑sized enterprises

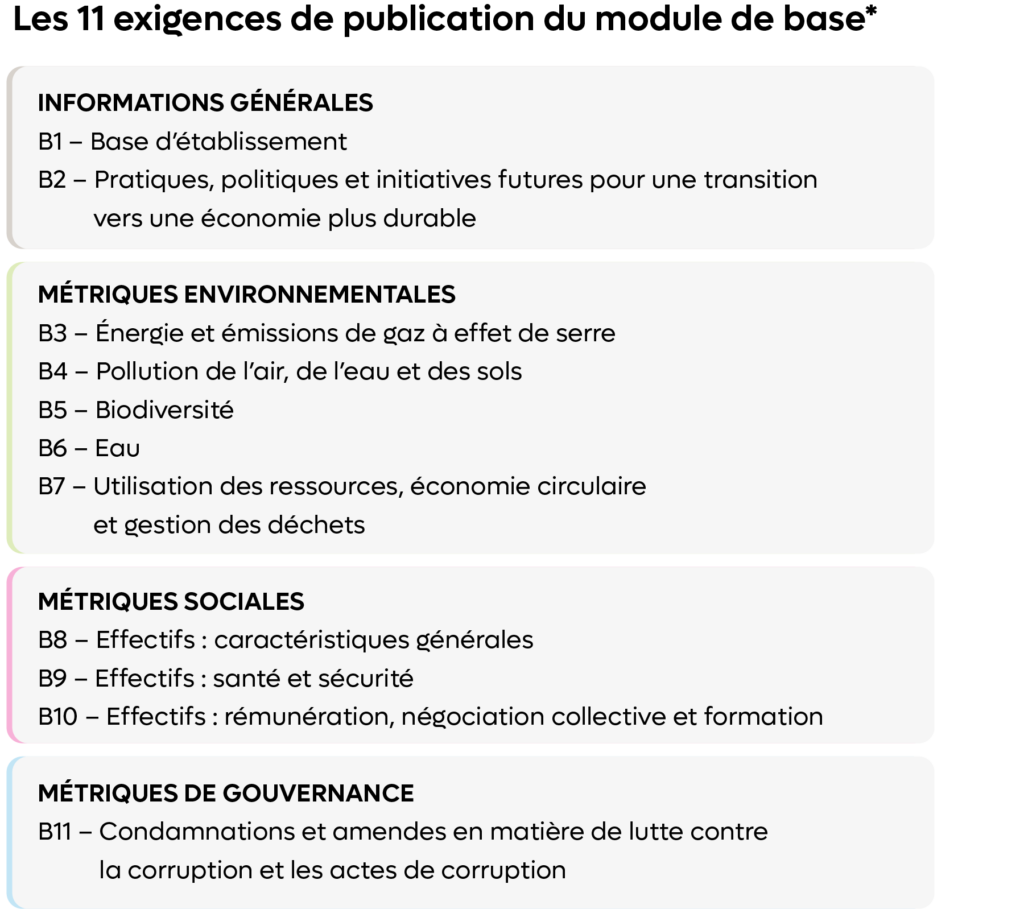

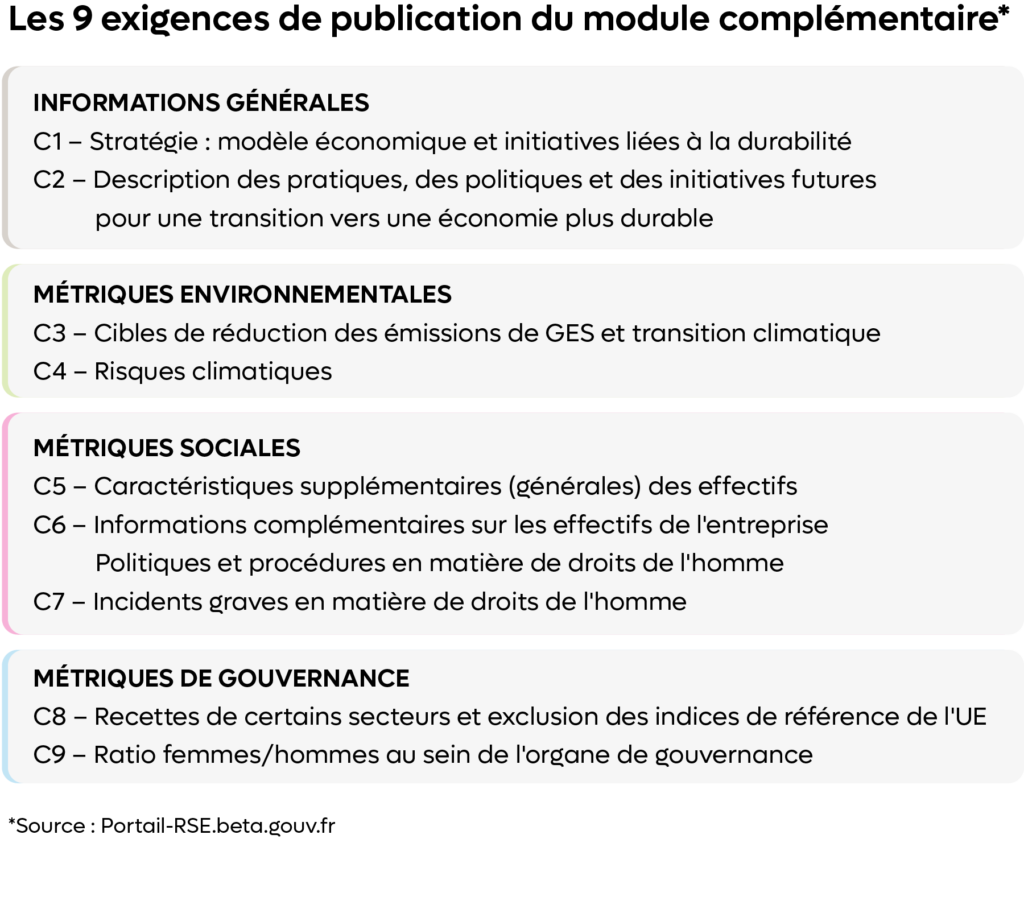

The VSME standards are structured around two modules:

- A core module, which serves as a key entry point for organisations seeking to structure their ESG reporting. It is based on a principle of applicability: companies disclose only what is genuinely relevant to their activities.

- A complementary (optional) module designed for organisations with a more advanced level of CSR maturity or those required to meet more sophisticated expectations from their partners.

Why adopt the VSME standards now?

To accelerate sustainable performance and take concrete action towards positive impact, Willing recommends adopting these standards without delay. Indeed, very small enterprises, SMEs and mid‑sized companies that embrace this voluntary framework can derive tangible benefits:

- Time and productivity gains: a single standard to address the various expectations of partners, resulting in a significant reduction in time and effort.

- Easier banking relationships and improved access to finance: VSME provides financial partners with standardised and comparable information. It also supports access to sustainable finance instruments, such as Sustainability‑Linked Loans (SLLs).

- A competitive advantage to strengthen market positioning: publishing a report aligned with the VSME format enables companies to showcase their CSR commitments to clients, investors and business partners.

- Anticipation of the expectations of CSRD‑in‑scope companies: organisations already subject to the CSRD require sustainability data from their partners in order to feed their own sustainability reporting. Furthermore, as small and medium‑sized companies continue to grow, they may eventually fall within the scope of the CSRD. Having an existing VSME‑aligned report will significantly ease future compliance with the regulation.

Willing supports companies on their sustainability journey

At Willing, we encourage organisations to take a proactive approach by anticipating regulatory changes, upskilling their teams, and engaging in ongoing dialogue with both internal and external stakeholders.

We firmly believe that the VSME standard has the potential to become a reference framework for all companies not subject to the CSRD, ultimately replacing the proliferation of disparate ESG questionnaires.

To successfully publish your sustainability report in line with the VSME standards, our support is built around three structuring steps:

1. Our conviction: double materiality as the starting point

We prioritise the double materiality approach which, although optional under VSME, provides a comprehensive assessment of a company’s positive and negative impacts, risks and opportunities—both of the company on the planet and of the planet on the company. This approach goes beyond compliance-driven reporting by enabling the development of a genuine sustainability strategy.

2. The sustainability report: a lever for transformation

We position the sustainability report as a tool for transformation. The business model, internal organisation, stakeholders, value chain and internal policies all become levers to strengthen performance and maximise the organisation’s social and environmental impact.

3. Progressive deployment, grounded in operational reality

We support our clients throughout every stage of implementing the VSME framework, from the initial diagnostic to the drafting of the final report. Working closely with executive and CSR teams, we remain closely attuned to their challenges and priorities, supported by our strong regional presence.

At Willing, we believe that a company’s value is measured as much by its financial performance as by its direct impact on society and the planet. This conviction underpins our commitment to supporting the integration of voluntary standards, so that we can move forward together towards a more virtuous economic system.

For further information, please do not hesitate to contact us.